The Global Reporting Initiative (GRI) is an international, independent not-for-profit organization that provides widely-adopted sustainability reporting standards. Over 10,000 companies participate in GRI reporting across more than 100 countries. Since launching its reporting standards in 1999, GRI’s mission has been to advocate for the broad adoption of high-quality sustainability reporting. GRI reporting is voluntary but enables diverse companies to be more transparent about their economic, environmental, and social impacts. Reporting under the GRI Standards helps organizations understand and communicate their impact on a wide range of sustainability issues, like climate change, resource use, human rights, occupational safety, data privacy, community development, and more.

GRI was founded following the Exxon Valdez oil spill in 1997 by Ceres and the Tellus Institute, with later involvement of the United Nations Environmental Programme (UNEP). Today, GRI reporting is a sustainability and transparency tool for business partnerships under the UN Global Compact. It allows companies to use their GRI reports for their UN Global Compact’s annual communication of progress (CoP). As one of the first disclosure tools, it’s aligned with many newer disclosure mechanisms, like the Task Force on Climate-related Financial Disclosures (TCFD) and many other business-focused sustainability reporting guidelines. The GRI Standards also support companies reporting progress against the UN Sustainable Development Goals. In fact, GRI partnered with the UNGC to develop the SDG Action Platform.

Sustainability and the GRI

GRI sustainability reporting helps companies become self-aware and better communicate their sustainability performance. As sustainability reporting transitions from “nice to have” to “must-have,” companies using GRI standards have the opportunity to review and consider sustainability in their annual risk assessments and transparency for investors, customers, and B2B partners.

GRI provides a modular reporting system with criteria for different sectors and topics. It requires companies to focus their reporting on specific material topics and allows them to compare their performance against others in their sector. In short, GRI helps companies gauge if their sustainability goals align with their practices.

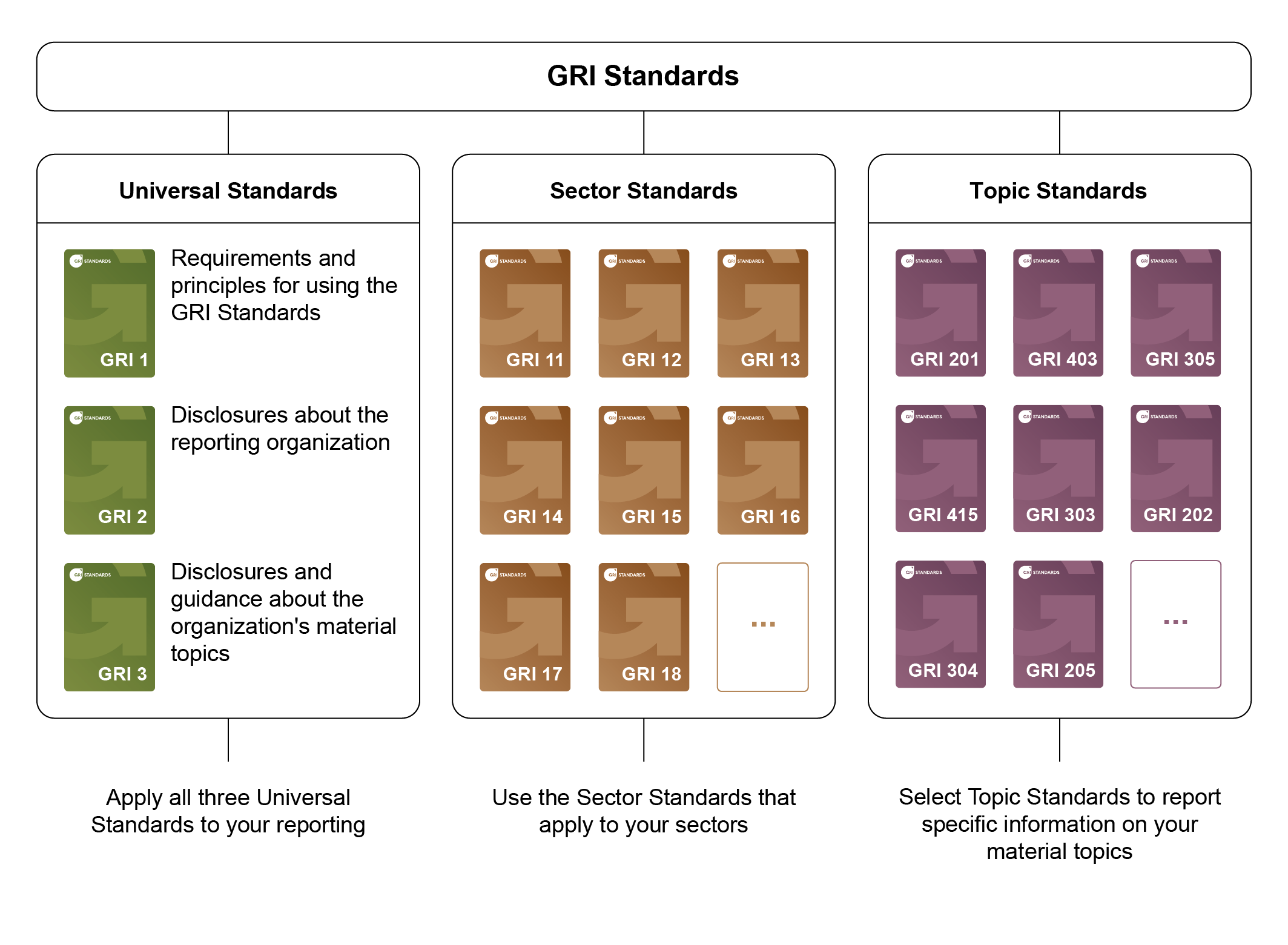

The three GRI reporting standards

The GRI publishes verifiable and comparable sustainability reporting standards. Companies typically disclose annually, some every other year. Disclosure of the reporting frequency is required by GRI, but companies have the option to share their reports on the GRI website. This allows companies in the same sector to compare performance and elevates corporate transparency.

GRI reporting starts with General Disclosures. This outlines a company’s reporting principles and sets the stage for the three reporting standards: Universal, Sector, and Topic Standards. All companies do the Universal Standards, the Topic and Sector standards are done as additional reporting criteria. The Universal Standards include core sustainability considerations around a company’s impact on the economy, society, and the environment. These standards include all foundational content. All participating companies report on Universal Standards. Companies then have the option to report on their specific sector or across different topical areas. By offering companies malleable, modular, interconnected standards, the GRI allows companies to home in on areas of greatest concern.

Currently, GRI focuses on the sectors with the greatest environmental impact, like fossil fuels. Topic standards represent all the potentially material topics compiled by GRI. Companies select disclosures from Topic Standards based on their Material Assessments. Once reports are complete, companies can make reports publicly available on the GRI website or opt for a third-party review. Third-party assurance becomes a required reporting step for companies opting in. GRI Standards and reporting criteria are reviewed every three years by the Global Sustainability Standards Board (GSSB), an independent body created by GRI.

Who can use the GRI Standards?

Any organization or company, private or public, of any size or geography can participate in GRI reporting, and the standards are available in twelve languages.

Overwhelmingly, the GRI Standards have emerged as the preferred reporting tool among top companies. A KPMG report on sustainability reporting tools in 2022 showed that 78% of the world’s 250 largest companies published GRI reports, up from 73% in 2020. 96% of the top 250 listed companies report on their ESG and sustainability activities. And in recent years, GRI reporting has seen an uptick in Saudi Arabia, the UAE, and India.

80% of companies using the GRI Standards disclosed their emissions across scope 1, scope 2, and scope 3 categories. While there is a diversity of sustainability reporting tools, the GRI—and other reporting mechanisms—now allow companies to link their GRI reports to their CDP and SASB disclosures, enhancing uniformity of sustainability disclosures for companies.

GRI reporting can be used as a way to assess diverse company activity. The EU requires sustainability reporting across financial and non-financial indicators via the SFDR and the CSRD, covering the majority of large and medium-sized EU-based companies. These regulatory requirements involve comprehensive sustainability disclosures aligned with the GRI, like economic, social, and environmental indicators. Additionally, scope 1–3 emissions criteria are now a reporting requirement under these EU policies. The U.S. SEC has recently proposed a rule for reporting scope 1 and 2 and possibly scope 3 emissions for listed U.S. companies, with disclosures on climate risk exposure.

Steps in GRI reporting

Whether it’s the GRI or another reporting tool, all sustainability reporting is the culmination of many months—and sometimes years—of work. Sustainability reporting requires deep reflection into organizational strategy and operating practices, so it’s important to allow enough time for information gathering and engagement across your organization and with core external stakeholders. Before beginning a GRI reporting assessment, companies should consider and review all GRI reporting criteria and requirements, including the overall GRI reporting system.

Unless you have an abundance of time and data, start small. The GRI has a core reporting option, which only requires companies to disclose one KPI for each material issue. It’s vital to first identify material topics via a materiality assessment—these are the areas where a company’s activities have the most significant impacts on the environment, economy, and people. Once you identify these materiality topics, companies set their sustainability priorities with stakeholders to better determine which material topics to include or exclude from their reporting.

During the reporting phase, all companies begin with the Universal GRI Standards. If applicable, companies can contribute to their sector-specific GRI reports, followed by optional Topic reporting criteria. Topics include disclosures on climate change, water, taxes, labor practices, and waste, among others. It’s important to consider early on which modular options your company will do. This will help set the stage for your overall scope, timeline, the stakeholders to involve, and decide whether or not this is something you’ll need to outsource.

Once reports are complete, companies can make their reports publicly available and submit them for review. All reports must include a searchable index. Should a reporter choose not to disclose specific criteria, they can indicate the reason. Reports with these types of exclusions are still considered complete. All can be made available on the GRI website and undergo a third-party assurance and review.

Learn how Sustain.Life can be your company’s reporting platform

Request a demo

The three GRI Standards explained

The GRI Standards consist of three series of standards: Universal, Sector, and Topic Standards. The Universal Standards contain a set of general disclosures that are mandatory for all reporters. Sector Standards contain additional disclosures for certain sectors. GRI has prioritized Sector specific standards for the highest-impact industries first: oil and gas, coal, as well as agriculture, aquaculture, and fisheries. Sector standards for the mining industry are currently being developed, with financial and textile industries to follow later in 2023. Topic standards list disclosures for a wide range of potentially material topics, though companies that have identified topics not listed by GRI must also report on those.

Within GRI reporting, Universal Standards are the starting point for all those reporting. These standards were updated in 2021 to better enhance reporting criteria and to reflect new sustainability reporting requirements in the EU. These standards include core indicators across environmental, social, and economic impacts. Sector standards are done if applicable for said business, Topic-specific reporting is optional.

Benefits and shortfalls of the GRI

While it might sound contradictory, GRI offers companies a set of adaptable standards for unique circumstances and impacts while also requiring a standardized set of disclosures from all companies. Increasingly, sustainability reporting is becoming a regulatory requirement rather than a voluntary expression of a company’s sustainability performance. With new regulatory requirements emerging from the EU and U.S., GRI reporting allows companies to meet stakeholder expectations and be prepared for mandatory reporting.

While the GRI is prized as an adaptable reporting mechanism, reports are not standardized beyond the Universal Standards. That means reports across different sectors may not be entirely comparable. Sector and Topic standards are based on the specific sector or material assessments. So the entirety of a company’s impact across different indicators may not be fully appreciated or entirely comparable to companies, even companies in the same sector.

Why is the GRI important for business?

GRI provides a common language and approaches for organizations to report on their sustainability performance, allowing for easier comparisons and benchmarking, as well as a set of adaptable and modular reporting standards.

Additionally, many sustainability-centered certifications, like B Corp, have begun working with GRI to collaborate on standards and sustainability. Companies that report in accordance with the GRI Standards benefit from a myriad of reputational, management, and regulatory requirements, like enhanced reputation, sustainability-centered decision-making, investor interest, (potential) regulatory compliance, and improved stakeholder relations.

As sustainability reporting across both financial and non-financial indicators increasingly becomes a requirement for businesses, it’s important to consider voluntary reporting in accordance with the GRI Standards to enhance sustainability, minimize risk, and establish sustainability policies and practices before they become a required for doing business.

Sources

1. GRI, “About GRI,” https://www.globalreporting.org/about-gri/ Accessed May 24, 2023

2. GRI, “Our mission and history,” https://www.globalreporting.org/about-gri/mission-history/ Accessed May 24, 2023

3. GRI, “Why report?,” https://www.globalreporting.org/how-to-use-the-gri-standards/ Accessed May 24, 2023

4. GRI, “Standards development,” https://www.globalreporting.org/standards/standards-development/ Accessed May 24, 2023

5. KPMG, “Big shifts, small steps Survey of Sustainability Reporting 2022,” https://assets.kpmg.com/content/dam/kpmg/se/pdf/komm/2022/Global-Survey-of-Sustainability-Reporting-2022.pdf Accessed May 24, 2023

6. GRI, “Four-in-five largest global companies report with GRI,” https://www.globalreporting.org/news/news-center/four-in-five-largest-global-companies-report-with-gri/ Accessed May 24, 2023

7. GRI, “Linking GRI reporting to other requirements,” https://www.globalreporting.org/how-to-use-the-gri-standards/global-alignment/ Accessed May 24, 2023

8. GRI, “A Short Introduction to the GRI Standards,” https://www.globalreporting.org/media/wtaf14tw/a-short-introduction-to-the-gri-standards.pdf Accessed. May 24, 2023

9. GRI, “GRI Report Services Methodology,” https://www.globalreporting.org/media/wrthwegq/gri-standards-alignment-check-services-methodology.pdf Accessed May 24, 2023

10. GRI, “Sector Program,” https://www.globalreporting.org/standards/sector-program/ Accessed May 24, 2023

11. B Corp, “GRI and B Lab team up on impact management,” https://www.bcorporation.net/en-us/news/press/gri-and-b-lab-team-impact-management-0/ Accessed May 24, 2023